Summary:

Replace Semilog monetary policy in sUSDe-long-v2 LlamaLend market on mainnet with this EMAMonetaryPolicy.

Abstract:

The EMAMonetaryPolicy is identical to policy contracts used by the sfrxUSD, sDOLA, and sreUSD lend markets. The defining feature of this policy is its dynamic rate adjustment at a target utilization based on the APR of the underlying collateral. It takes min/max multipliers, target utilization, and rate shift as arguments and applies an EMA moving average to the dynamic rate adjustment.

Motivation:

Yieldbearing stable markets are sensitive to the lend market rates, requiring predictable correlation with changes in yield on the underlying collateral. Markets using EMAMonetaryPolicy can improve performance by stabilizing the rate spread for borrowers and improving returns to lenders. This is due to the configurable target utilization and relatively high reliability that the market will operate close to the target range. Markets using this policy have not experienced concerning levels of illiquidity, but have been observed to maintain a consistently high level of utilization compared to Semilog markets.

Specification:

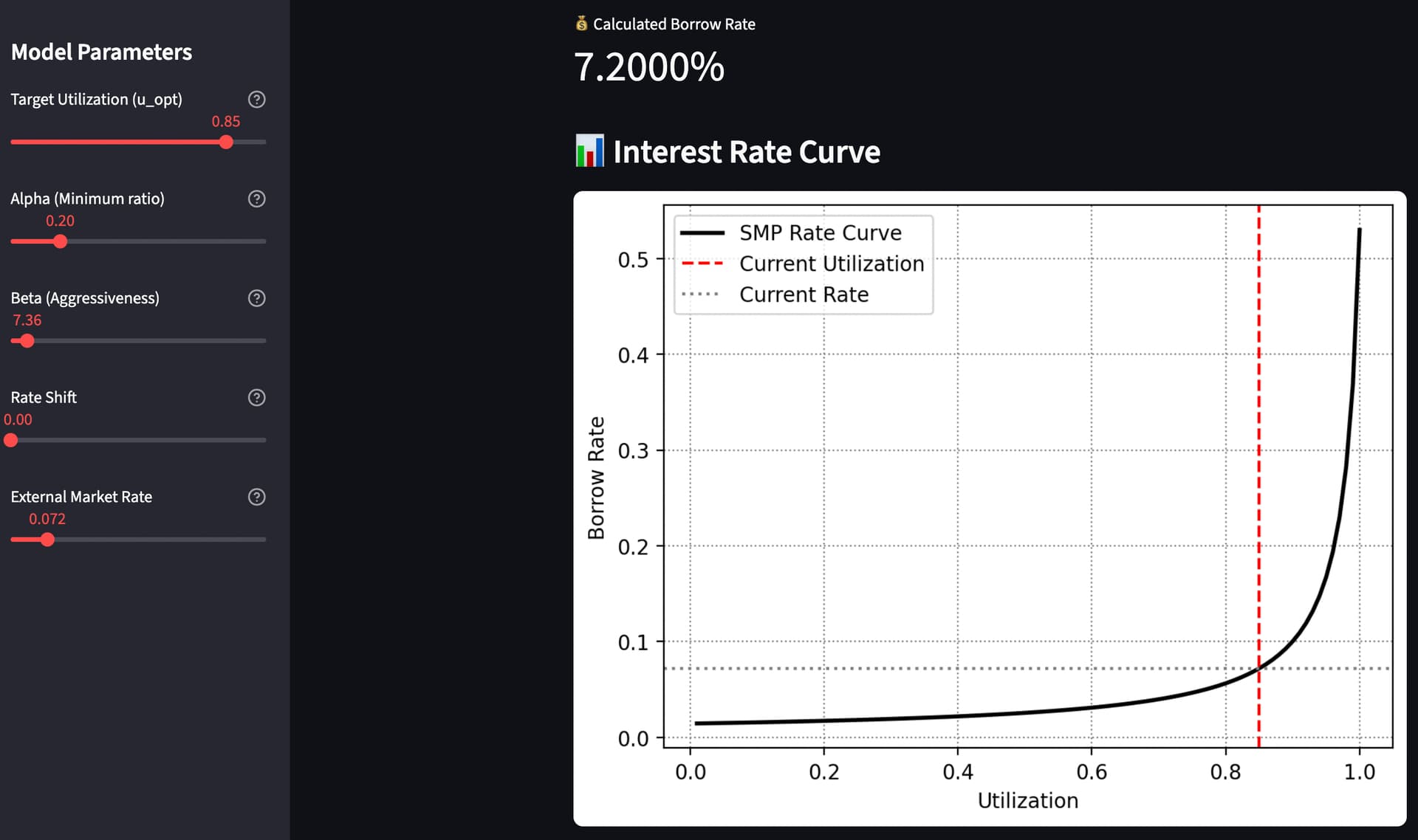

The MonPol is set with parameters identical to markets in prod:

| Param | Value |

|---|---|

| Low Ratio (Alpha) | 0.2 |

| High Ratio (Beta) | 7.2 |

| Target Utilization | 85% |

| Rate Shift | 0 |

Assuming the sUSDe APR, as calculated by the RATE_CALCULATOR, is 7.2%, the borrow rate at 85% utilization will be the same. The rate at 0 utilization is 1.4% and at max is 51.8%. The values will shift dynamically as the sUSDe APR changes.

Vote Actions

ACTIONS = [

# Set sUSDe MonPol

(CONTROLLER, "set_monetary_policy", "0xe60659e76056e3736dffb6981c289df55567395b"),

]