Summary

This report outlines the activity of LlamaRisk for Q2 of 2025 (April - June). LlamaRisk conducts research and risk management processes for all Curve products, for which we have been pursuing several research verticals. Our applied research includes a debt ceiling methodology for identifying collateral integrity, an interest rate model optimization methodology for enhancing lend market performance, and AMM optimization techniques, including simulations and order flow analysis.

Over this quarter, we have particularly emphasized ensuring the stability of crvUSD and leading integrations support for LlamaLend markets. We work closely with asset issuers to deploy and bootstrap their markets, and we have made improvements to LlamaLend design features in terms of monetary policies, oracle implementations, and the introduction of the oracle proxy.

Some of the main highlights include:

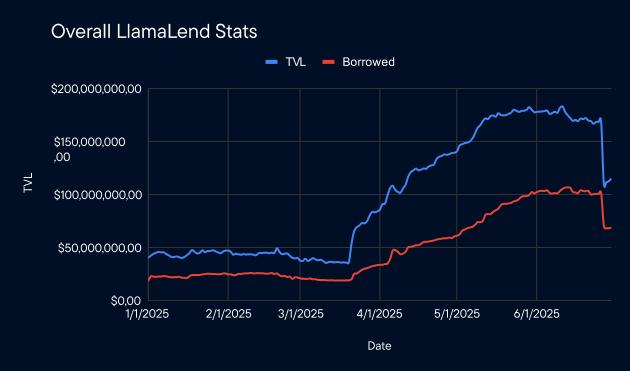

- LlamaLend markets saw an increase in TVL by 34% over the quarter (April 1 - June 31) and open borrows increased by 104.5%,

- Average PegKeeper debt rose, resulting in the most stable quarter yet for the crvUSD peg,

- A new EMAMonetaryPolicy successfully improved lend market performance for yieldbearing stable markets and ProxyOracle improved the flexibility of lend markets,

- Optimism LlamaLend markets and supporting AMMs were bootstrapped on behalf of Curve with a grant procured by members of LlamaRisk and Swiss Stake through the LlamaBoost Foundation.

The LlamaRisk team remains hard at work to secure the Curve ecosystem and is grateful for the abundant community support.

Governance Activity

LlamaRisk strives to engage the Curve community through our commitment to transparent and diligent governance activity. We aim to give a thorough explanation for all proposals, supported by qualitative and quantitative analysis. Our governance activity offers a lens into the depth of our research and a rationale for the recommendations we make to the DAO.

LlamaLend Market Related Proposals

LlamaLend Proposal Summary

LlamaRisk has been applying our research on LlamaLend markets to mitigate risk and optimize markets for users. These activities include cleaning up markets with unsafe oracles, optimizing market parameters for utilization/stability, and bootstrapping new markets through gauge votes and Resupply proposals.

Highlights:

- Increase in crvUSD borrowed by 104.5%

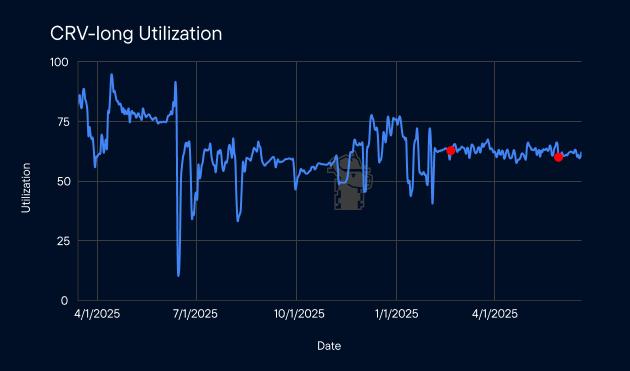

- Following two optimization proposals, the CRV-long market has exhibited more stable utilization.

- Introduced proxy oracles in LlamaLend market deployment, allowing the Curve DAO to change oracle implementation post-deployment

- Implemented EMAMonetaryPolicy in yield-bearing asset markets to enhance market efficiency, improving rates for lenders and improving rate predictability for borrowers.

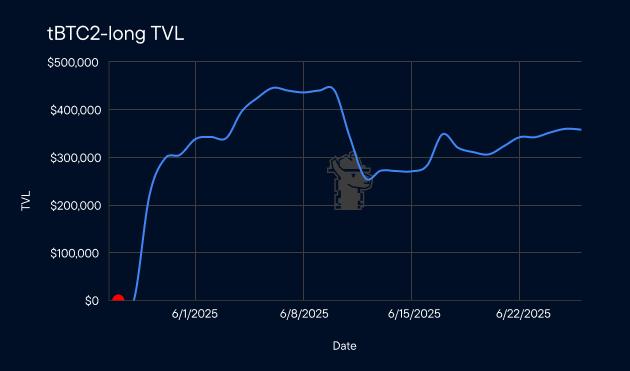

- Successfully bootstrapped tBTC2-long and sUSDS-long LlamaLend markets

| Post Date | Description | Execution Date |

|---|---|---|

| 4/14/25 | Set Llamalend Min/Max Market Rates on Optimism (OP, CRV, WBTC, ETH, wstETH) | 4/21/25 |

| 4/19/25 | sUSDS-long Llamalend Market Gauge Vote and Analysis | 4/29/25 |

| 5/16/25 | Add Gauge for sUSDf-long Llamalend Market | 5/26/25 |

| 5/9/25 | Onboard tBTC2-long Llamalend Market to Resupply | 5/27/25 |

| 5/9/25 | Onboard sUSDS-long Llamalend Market to Resupply | 5/27/25 |

| 5/19/25 | Adjust CRV-long Llamalend Market Rates | 5/31/25 |

| 5/24/25 | Set New EMAMonetaryPolicy on sfrxUSD-long Llamalend Market | 6/4/25 |

| 5/27/25 | Kill Gauges for Llamalend Markets with Unsafe Oracles | 6/9/25 |

| 6/19/25 | Set EMAMonetaryPolicy on both sDOLA-long LlamaLend Markets | 6/27/25 |

Key Metrics

The total amount of crvUSD that was borrowed across LlamaLend markets increased by ~104.5% from $33.54m to $68.66m in Q2 of 2025. A maximum increase of 218% (106.63m borrowed) was achieved in mid-June. Additionally, the average LlamaLend TVL in Q2 was $151m, which is a 228% increase from $46m in Q1.

As part of a multi-proposal initiative, LlamaRisk has continuously optimized parameters for the CRV-long LlamaLend market, beginning on 2/19/25 with a follow-up proposal on 5/31/25. Using data from 1/1/25, the standard deviation of utilization decreased from 7.96% to 1.94% after proposal execution on 2/19/25, indicating greater market stability. Average utilization rose from 40.5% to 62.5%, approaching the 65% target. While these improvements suggest effective intervention, external factors may have contributed, as CRV price volatility also declined (standard deviation fell from $0.18 to $0.12). The updated target utilization of 82%, introduced on 5/31/25, is part of a larger, multi-step process that requires multiple market rate proposals to pass. View the full plan for CRV-long market rates here.

Red dots signify proposal executions.

LlamaRisk changed the monetary policy on the sfrxUSD-long LlamaLend market from Semilog to a new EMAMonetaryPolicy. This monetary policy uses the underlying APY of the yieldbearing collateral to determine a borrow rate at target utilization. This has several advantages, such as automatically conforming the borrow rate for leveraged looping strategies and increasing market efficiency. Since the sfrxUSD-long monetary policy was changed, utilization has settled around the target of 85%. As expected, the borrow APY for sfrxUSD shows a stronger correlation with its underlying APY than comparable markets. Since 6/4/25, the correlation between sfrxUSD-long borrow APY and its underlying APY has been 0.4, compared to 0.27 for sUSDe, and -0.54 and -0.09 for sDOLA-long and sDOLA2-long, respectively.

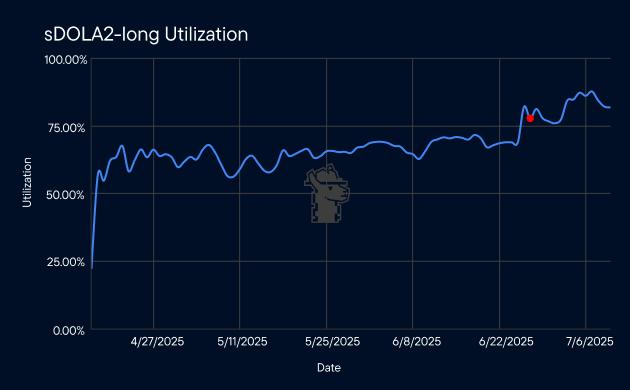

LlamaRisk introduced a proposal to switch both sDOLA markets to the EMAMonetaryPolicy, as the current negative correlations indicate an undesirable dynamic: borrow APY decreases when the underlying APY rises. This proposal passed on 6/27/25, and already an immediate effect can be seen on the sDOLA2-long market where the utilization pushed towards the target utilization of 85%. Even during the wstUSR Resupply exploit, neither sDOLA markets or the sfrxUSD market experienced a prolonged period of illiquidity with utilization staying below 90%.

Red dot signifies proposal execution.

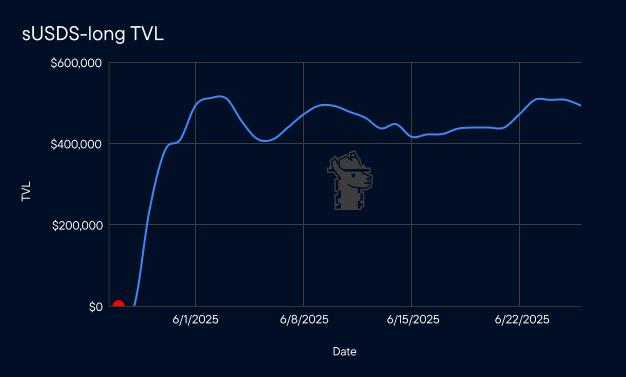

LlamaRisk successfully bootstrapped the tBTC2-long and sUSDS-long LlamaLend markets through the launch of Resupply markets. Following the launch of tBTC and sUSDS Resupply markets on 5/27/25, TVL in the respective LlamaLend markets skyrocketed, with both markets moving from $0 to over $200k in the following days.

Red half circle signifies proposal execution

crvUSD Related Proposals

crvUSD Proposal Summary

LlamaRisk has been active in securing the stability of crvUSD through modifying the PegKeeper and monetary policy. Since the USDM depreciation was announced, LlamaRisk has passed three proposals to remove USDM from the PegKeeper and wind down USDM usage in Curve. Now, there is a publicly available Curve Risk Portal which includes LlamaRisk’s Debt Ceiling Methodology. This methodology was employed to optimize the LBTC mint market.

Highlights:

- Daily standard deviation of crvUSD peg decreased by 66%

- The crvUSD average price moved 48% closer to peg

- The average PegKeeper share of total debt rose by 71% QoQ

- The average supply of scrvUSD increased by 67% QoQ

| Post Date | Description | Execution Date |

|---|---|---|

| 4/3/25 | Switch weETH MP, Reduce Rate Shift on Yielding crvUSD Markets, Increase TargetFraction, Increase Total PegKeeper Debt Ceiling | 4/10/25 |

| 5/12/25 | Remove USDM from Pegkeeper and crvUSD Price Agg | 5/19/25 |

| 5/22/25 | Set USDM PegKeeper Action Delay to 0 | 5/28/25 |

| 5/22/25 | Increase LBTC Mint Market Debt Ceiling | 5/31/25 |

| 6/6/25 | Fully Deprecate USDM Pegkeeper | 6/16/25 |

Key Metrics

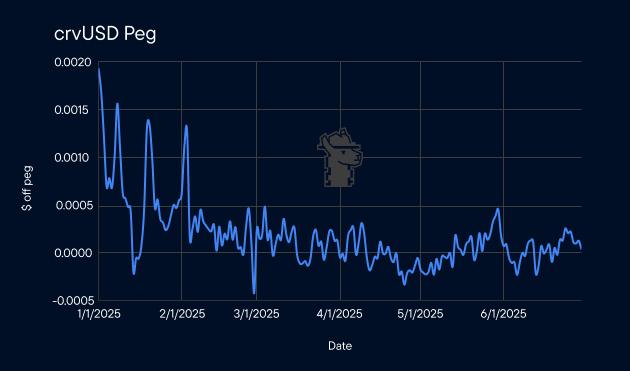

crvUSD saw its strongest peg in Q2 of 2025. The daily standard deviation of the peg dropped from $0.00047 to $0.00016 - a reduction of 66%. This depicts a drastic decrease in peg volatility. Additionally, the crvUSD improved to an average of 3.9 BPS off-peg, a reduction from 7.5 BPS the previous quarter.

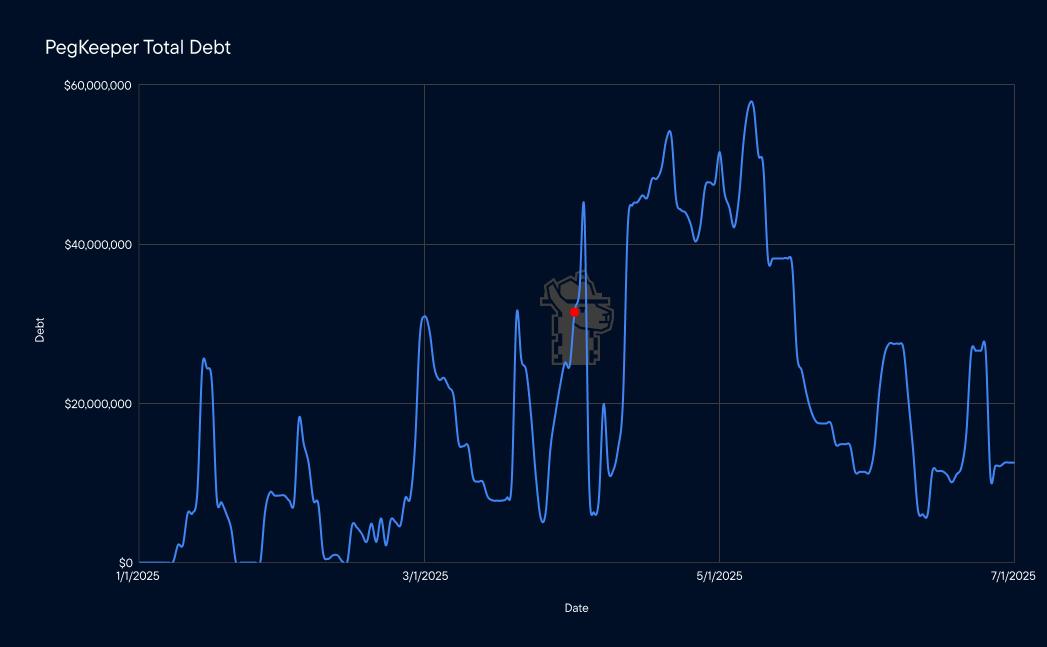

Average PegKeeper debt and its share of total debt both increased in Q2. The average PegKeeper debt rose from $9.7m in Q1 to $28m in Q2. Its share of total debt rose from 14% to 24%. This PegKeeper debt acts as a buffer to keep the crvUSD peg resilient to changing borrower behaviors and fluctuations in demand for crvUSD. We consider it desirable to maintain some PegKeeper debt to regulate borrow rates and provide a consistent buffer for borrowers to open positions.

Red dot signifies start of Q2

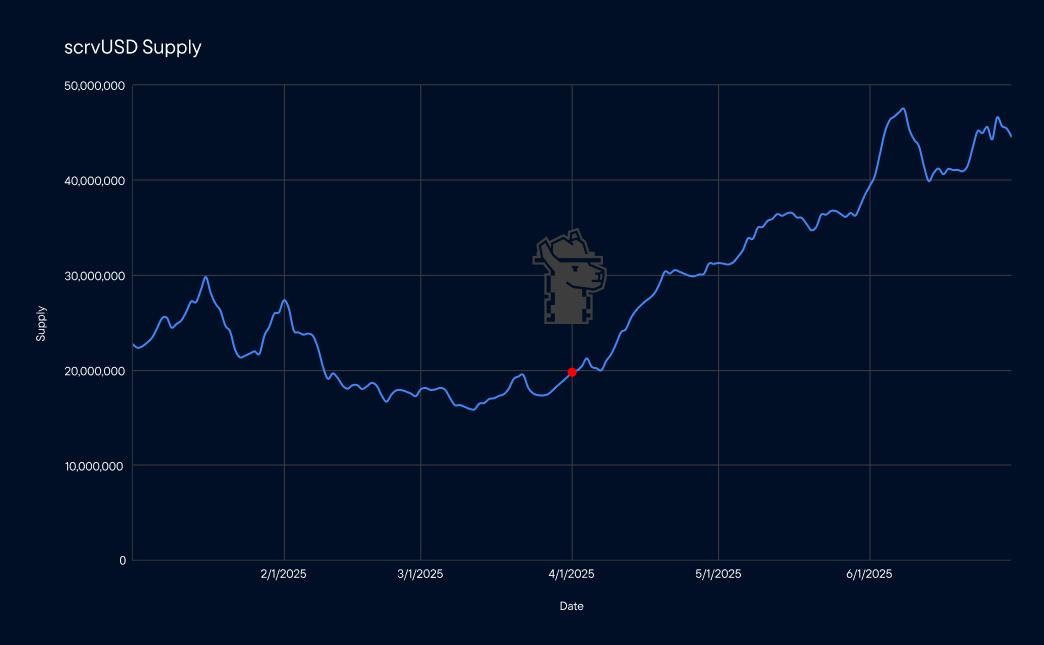

The average supply of scrvUSD also increased from Q1, moving from 21m to 35m - an increase of 67%. scrvUSD is a supply sink for crvUSD, creating demand for the stablecoin that supports the peg and regulates borrow rates.

Red dot signifies start of Q2

AMM Related Proposals

AMM Proposal Summary

LlamaRisk has been actively managing AMM pools, primarily by working with asset issuers to deploy and optimize pools, killing gauges to deprecated pools, and optimizing parameters in pools of interest. All parameter actions we make on AMM pools involve coordination with the protocol team to ensure the action aligns with the team’s objectives for the pool.

Highlights:

- Following parameter optimization, average daily pool utilization increased by 50% for DOLA/USR and 66% for DOLA/sUSDe, while daily pool volume rose by 57% and 160%, respectively

- Average order flow share increased by 133% for DOLA/USR and 244% for DOLA/sUSDe.

- Provided analysis and onboarding support to StakeDotLink and f(x) teams for their AMM pools.

| Post Date | Description | Execution Date |

|---|---|---|

| 3/29/25 | Increase PayPool A to 5000 and Off-Peg Multiplier to 10x | 4/6/25 |

| 4/23/25 | Ramp A on all PegKeeper Pools from 500 to 2000 | 5/2/25 (2nd Vote) |

| 4/29/25 | Proposal to add LINK/stLINK-ng to the Gauge Controller | 5/6/25 |

| 5/20/25 | Kill USDM Pool Gauges | 6/4/25 |

| 6/2/25 | Kill Gauge Emissions to Pools with CVG | 6/10/25 |

| 6/11/25 | Ramp A on USDC/fxUSD pool | 6/18/25 |

| 6/14/25 | Ramp A on Several DOLA Pools | 6/23/25 |

| 6/19/25 | Add fxSAVE-long LlamaLend Market on Mainnet to Gauge Controller | 6/27/25 |

Key Metrics

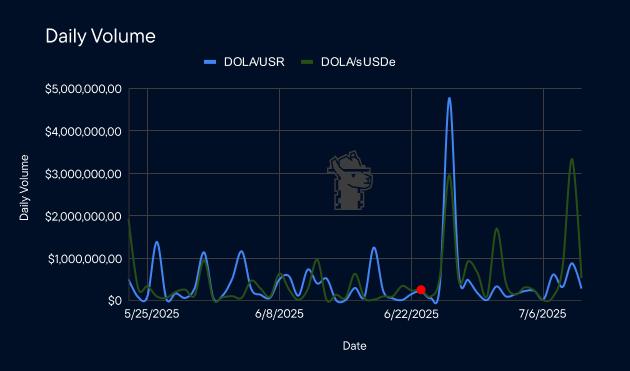

The latest A parameter optimization across four DOLA pools led to a notable increase in trading volume, particularly in the DOLA/USR and DOLA/sUSDe pools. For example, in the DOLA/USR pool, average daily volume rose from $350K to $550K when comparing the month before the proposal’s execution to the current period. The average daily pool utilization for the DOLA/USR pool also saw a jump from 1% to 1.5%. Comparing the same time periods, the DOLA/sUSDe pool jumped from $288k to $750k average daily volume. The average daily pool utilization also increased from 1.5% to 2.5%. The order flow analysis led to an increase in the average order flow share for both pairs — from 4.3% to 10% for DOLA/USR, and from 0.9% to 3.1% for DOLA/sUSDe.

Red circle signifies proposal execution

Misc Proposals

Misc Proposal Summary

Through offering OP incentives from a previous grant, LlamaRisk was able to successfully bootstrap both LlamaLend markets and select Curve liquidity pools on Optimism. LlamaRisk also introduced a proposal that allows any EOA or smart contract to lock CRV.

Highlights:

- LlamaLend markets receiving incentives had a TVL increase of 730% with incentivized pools seeing a 126% increase

- Multisigs can now lock CRV as veCRV and participate in Curve governance, and smart contract interactions are possible generally

| Post Date | Description | Execution Date |

|---|---|---|

| 4/7/25 | Bootstrap Optimism Llamalend Markets with 60k OP | 4/17/25 |

| 5/6/25 | Remove veCRV Whitelist | 5/26/25 |

Key Metrics

In the week following the launch of OP incentives, TVL in Optimism LlamaLend markets rose by 730%, while incentivized pools saw a 126% increase.

Red half circle signifies proposal execution

Plans for Q3

In the coming months, our plan is to expand on our R&D efforts related to crvUSD and LlamaLend. We collaborate closely with Swiss Stake, having weekly syncs on smart contract developments, especially those related to feature enhancements to the lend platform. Our view is that there is still much untapped potential in this Curve product and that it may emerge as a significant revenue driver for Curve by the end of year.

There are several research verticals we continue to explore:

- Interest Rate Optimization: We have published several reports on our methodology and analysis around interest rate optimizations and improved Monetary Policies for Curve. This research contributes to increased returns for lenders while improving assurances of maintaining liquid markets. We continue to make improvements in optimization monitoring and automation processes.

- Debt Ceiling Methodology: Our debt ceiling methodology considers liquidity conditions for the collateral, borrower behaviors in the market, global leverage conditions, and unique features of LlamaLend markets (e.g. LLAMMA liquidations) to determine a safe debt ceiling for each market. We have incorporated this analysis in our Curve Risk Portal for crvUSD mint markets and we are currently developing a streamlined dashboard where users can conveniently view the safeness of each market’s debt exposure, according to this methodology.

- AMM Optimization: We continue to refine simulations and order flow analyses across DEXs to identify opportunities for AMM optimization and determine appropriate parameterization. We also stress the importance of retrospective analysis to assess the effectiveness of the changes.

- Oracles R&D: This involves several areas of research regarding Curve oracles, including to monitor the health of Curve pools being utilized in lend and mint markets, and developing strategies for improving the resiliency of oracles in the markets. We consider this an important area of research that will become increasingly critical as lend market TVL continues to grow.

Another priority in the near term is to replace the PegKeeper that has recently been deprecated with a suitable stablecoin. While crvUSD can function perfectly fine with 3 PegKeepers, the PegKeeper design prefers at least 4 to optimally perform peg checks on its operations. We have been in discussion with Frax and Curve stakeholders about onboarding frxUSD, and we will soon be publishing a PegKeeper Onboarding Risk Report as a prerequisite to its onboarding.

We continue to perform our role as integrations support for asset issuers who are interested in creating or optimizing Curve pools and lend markets. Teams who are in need of assistance with market parameterization or deployment can always reach out to us; you can reach us at our public Telegram channel or feel free to dm @WormholeOracle.

We are pleased to observe a positive growth trajectory and stability of crvUSD over the past quarter, and the stable performance of the Curve AMM. Thank you to all DAO community members for your support and trust; we will be continuing our commitment to building user trust and are confident Q3 KPIs will reflect that commitment.