As Yield Basis safety checks and the launch process progresses, I propose to increase crvUSD cap for its pools to 300M crvUSD. This allows to have 3 pools (crvUSD/WBTC, crvUSD/cbBTC, crvUSD/tBTC) of 100M USD size each (up from the current 20M each), deposits of 3 x 50M USD in Yield Basis and working debt of 3 x 50M crvUSD in its smart contracts.

This is a required step before turning YB emissions on, 20% of which (75M YB tokens) are distributed from distribution smart contract controlled by Curve DAO. A vote for Curve DAO to utilize these tokens will be created with a separate proposal.

Safety information

Apart from audits with Chainsecurity, Statemind, Mixbytes, Electisec, Quantstamp and Pashov, Yield Basis runs a “crowd audit” with Sherlocks. There were good findings (to be summarized shortly) which were all addressed without redeploying any smart contracts after launch. In addition, mechanisms in the new generation of Curve pools had to be tweaked to prevent an “ape tax” on users who deposit too quickly one after each other.

None of the correct findings presented any risk for crvUSD allocation.

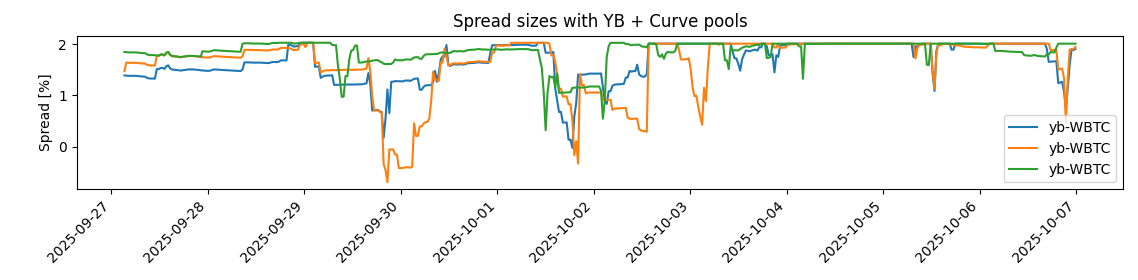

Apart from technical safety, one needs to consider economic safety. When liquidity pools are balanced - net pressure on crvUSD is zero. However in disbalance - there’s a non-zero second-order pressure. For example, imbalance of this WBTC/crvUSD pool is typically around 1.5%.

This means that 3 pools together currently create positive or negative pressures on crvUSD supply up to about 1M crvUSD. This is negligibly small in comparison with pressures exhibited by loans in LlamaLend.

With the above, I see it to be safe to expand the caps.

Protocol statistics

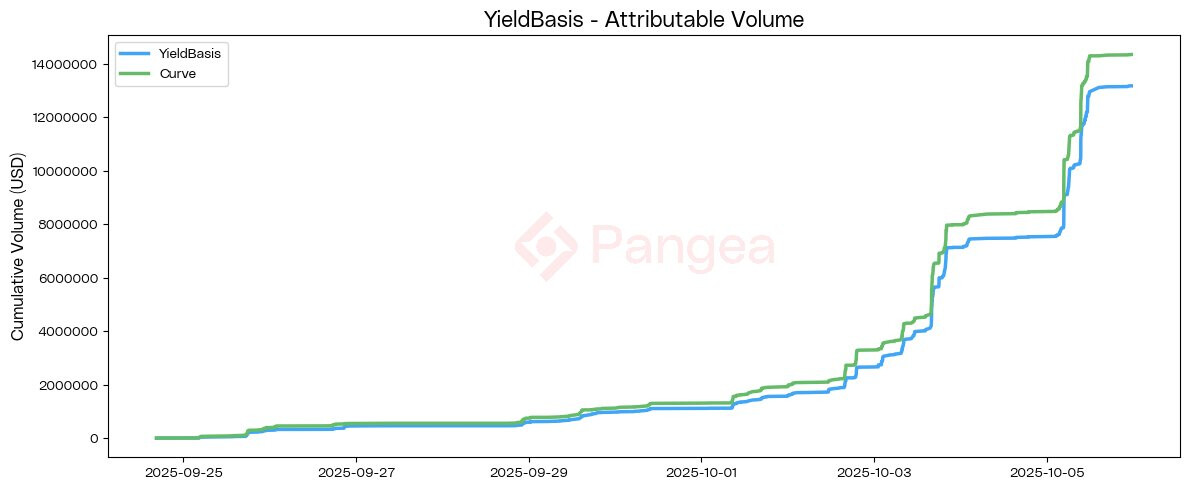

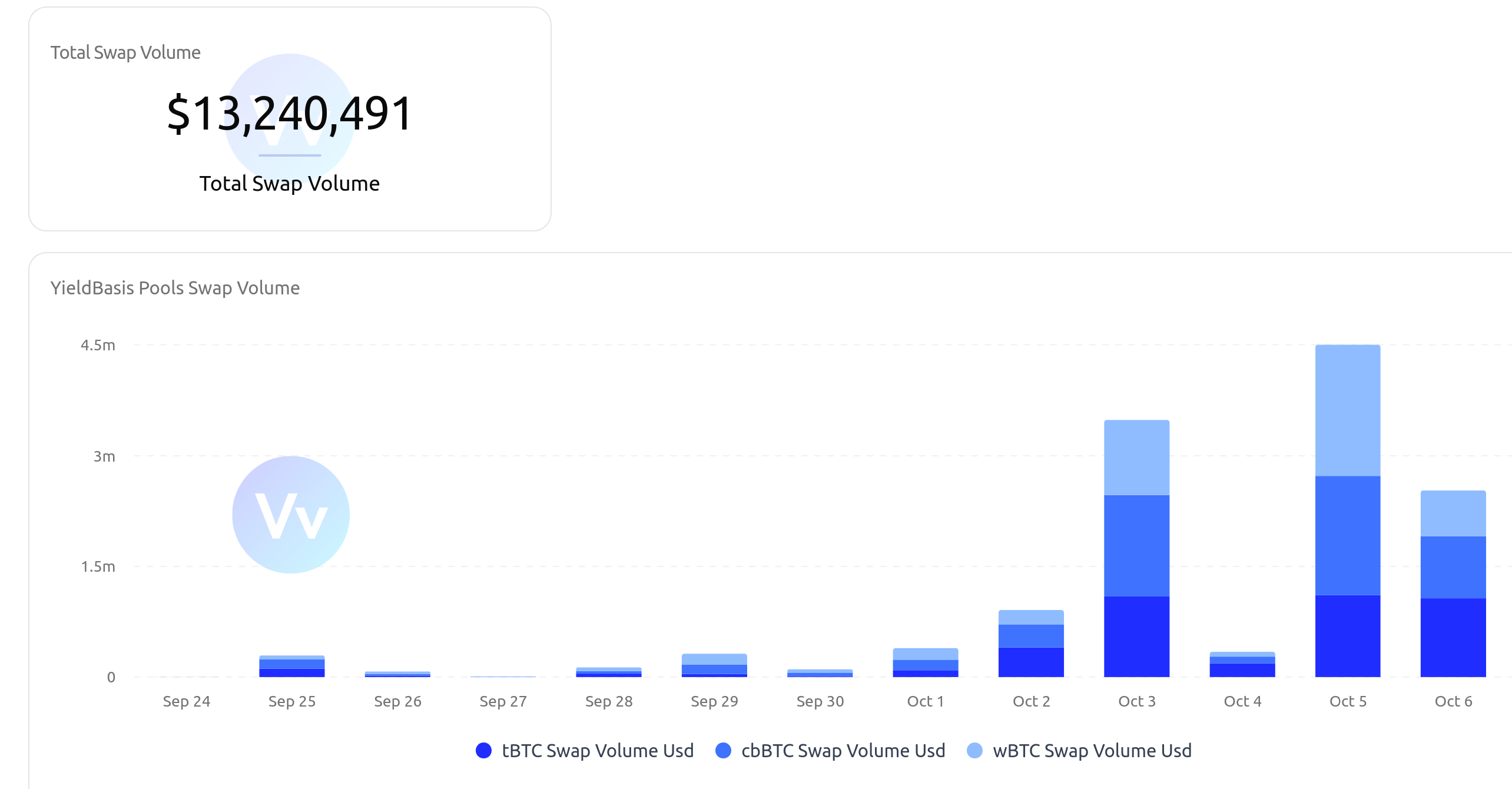

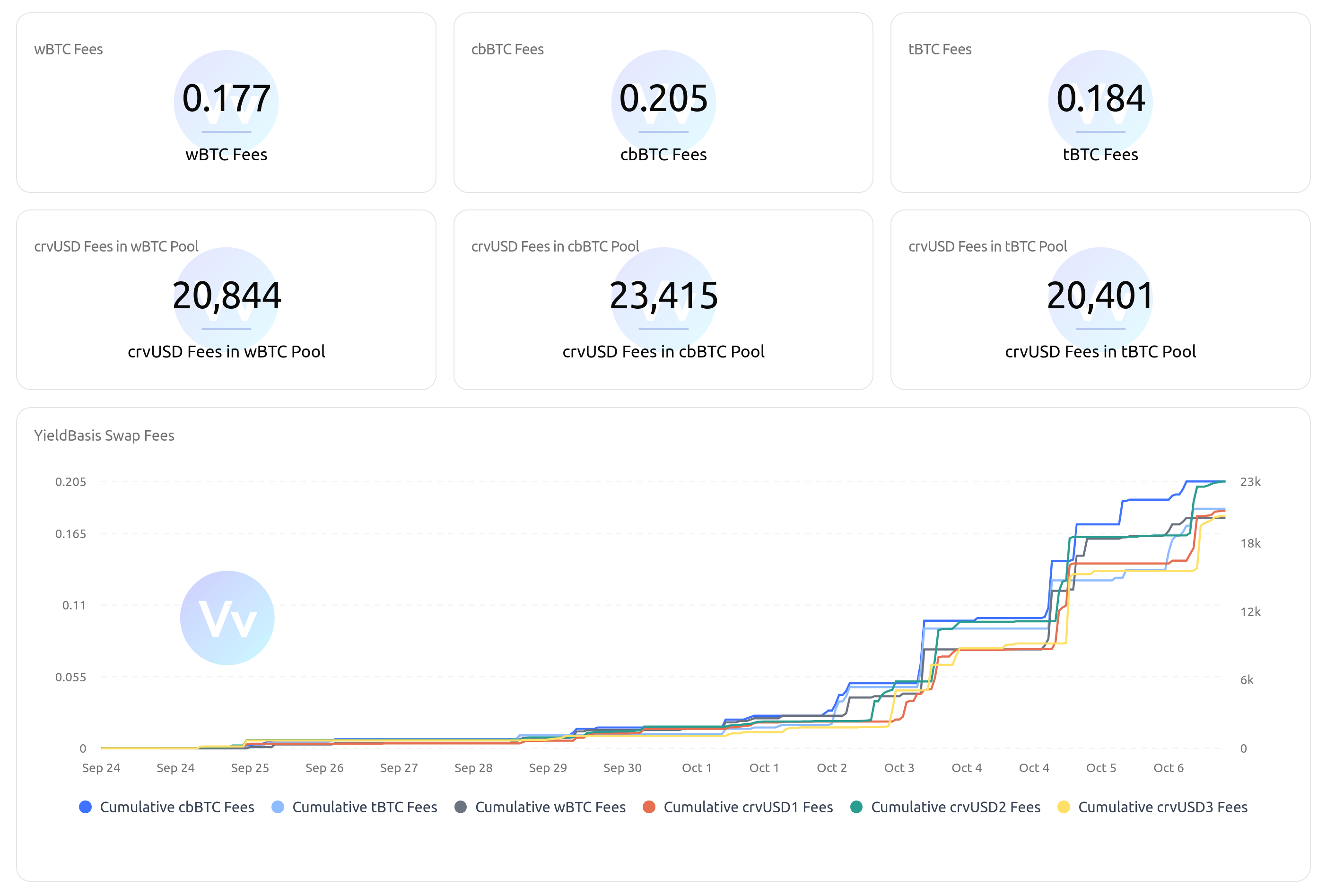

Trading volumes average to around 1M per day per pool at 20M pool TVLs while AMM fee is set to 1% (resulting in 2% spread). In addition, about 20% of this volume is happening in YB AMM which. Both of these volumes result in crvUSD swaps on Curve. Trading volumes done so far are 13M, as evidenced by statistics from ValueVerse.

Pool caps were filled in a minute after the first cap raise, getting total Curve pool TVL up to +60M USD.

Fees charged by Curve pools amounted for around 120k USD. Most of these fees were spent on pool rebalancing and releveraging.

Stable pools with crvUSD earned around 1.5k USD from crvUSD-stablecoin volumes in both Curve pools and releverage AMMs, and although veYB does not receive admin fees yet, it could have earned somewhere between 5k and 10k USD worth of Bitcoin-denominated tokens.

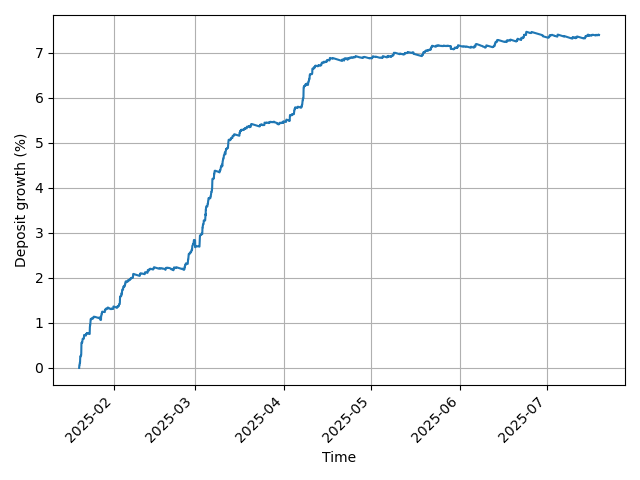

Simulations show that earnings could not have been significant after mid-April assuming that all trading volumes come from arbitrage only.

However, it appears that natural volumes from Cowswap, Odos and Curve router are not insignificant, so Yield Basis works BETTER than predicted by simulations due to that. We need longer time to tell exact numbers on expected natural APRs due to data being inherently noisy.

Although YB AMM spreads are as big as 2%, the presence of the second AMM makes “effective spreads” smaller during volatility time. This ensures that Curve automatically steps in as a venue for swaps in volatile times. However, VirtualPools which use YieldBasis AMM should be integrated in Curve Router to fully benefit from that.