Summary

This is a follow-up on this proposal. Since its time, we’ve got more data and closed the value loop in Yield Basis with fee distribution on. It is time to execute on the proposal to increase the current 300M crvUSD credit line for Yield Basis to 1B crvUSD (which means up to 0.5B USD TVL in Yield Basis eventually).

Safe use of the credit line

Crucially, this 1B credit line will not be fully utilized upon approval. It acts as a maximum ceiling to be drawn upon over time. The allocation will remain unutilized in the contract, acting as a reserve that is adjusted weekly.

Actual usage is strictly data-driven and safety-focused:

- Dynamic Caps: Usage is dictated by “caps” which are adjusted weekly to match specific metrics, primarily Curve pool sizes.

- Governance Control: While Curve approves the total line, specific cap increases must be gradually voted in on the Yield Basis side.

- Initial Rollout: Based on the performance of YB incentives for crvUSD pools, it is safe to initially utilize only 80M crvUSD (increasing pool caps by ~$13.3M each).

- Future Growth: We will monitor the filling of main crvUSD pools (excluding liquidity created by PegKeepers) to identify safe possibilities for cap increases. We anticipate it taking several months to safely utilize the full credit line, including the potential creation of an ETH/staked ETH pool early next year.

crvUSD peg stability (update)

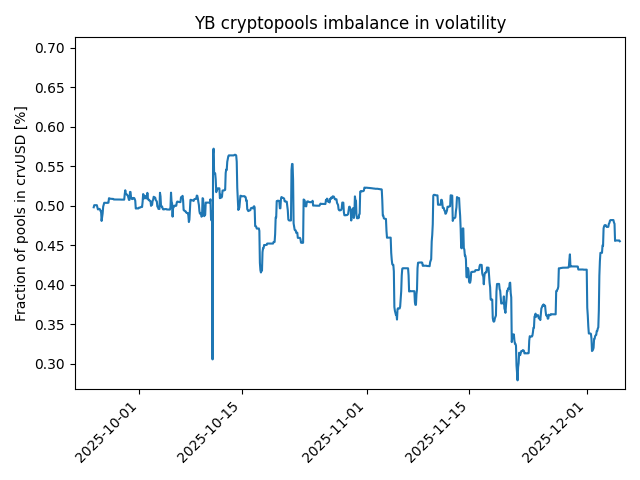

Observed BTC/crvUSD pool imbalances

Imbalances of *BTC/crvUSD pools play the key role in effects on crvUSD peg stability. It was measured that since the start of Yield Basis in September that the worst imbalance in total was around 30%/70% which means that 20% of net Curve pools size (or 40% of YB TVL size) of crvUSD price pressure was created in the worst case. The imbalance, and hence the amount of crvUSD to sit somewhere temporarily, is therefore equal quarter of the Curve pool size, or half of Yield Basis TVL size at worst S_{yb}/2.5.

Growth of crvUSD/stablecoin pools

A part of YB inflation given to Curve is currently streamed as incentives for USDC/crvUSD, USDT/crvUSD and frxUSD/crvUSD pools (the latter also gives extra incentives from Frax). These incentives buy votes for these pools.

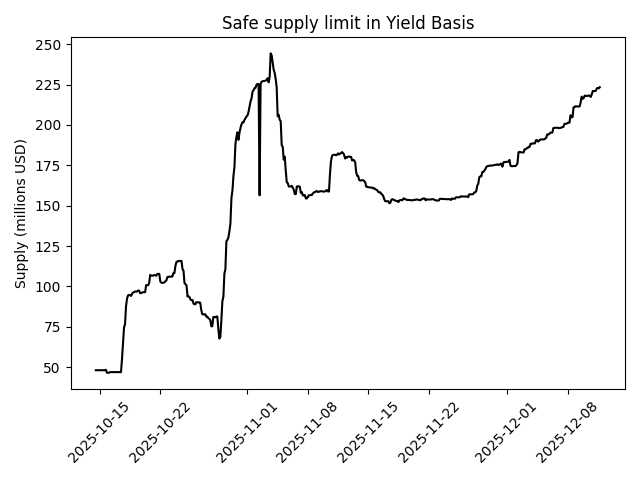

TVL of these stablecoin pools since credit line for Yield Basis was set to $300M is measured and shown on the graphs below:

Blue line stands for staked supply (driven by YB incentives mostly), and gray line is total supply (which is higher when PegKeepers mint crvUSD to deposit).

Over that time, TVL of key crvUSD pools just from YB incentives grew up from $26M to $102M at the time of writing.

What YB caps should be

When crvUSD/stablecoin pool of size p is created, it makes a supply sink for crvUSD of the size p/2: this gets absorbed by PegKeepers. It is reasonable to assume that pool can safely get as imbalanced as 30%/70% without much harm to liquidity density. This means that the amount of crvUSD which these pools can safely absorb, along with supply sinks they create, is 0.75\,p.

We already determined that YB TVL cap can be 2x of absorbable crvUSD, based on maximum imbalance. Therefore:

S_{\max}=2.5\times 0.75 \times 102~\text{(M USD)}\approx 190~\text{(M USD)}

This means that we are ready to increase the sum of caps by $40M currently (or utilize +80M crvUSD allocation). This number should be regularly updated and adjusted on a weekly basis.

Conclusion

- A vote to increase the current 300M crvUSD line of credit to Yield Basis Factory to 1B crvUSD will be created;

- After the vote goes through, a vote on Yield Basis to increase caps by 40M (subject to metrics of crvUSD pools at that time) will be created;

- Further utilization of this credit line will likely take some months and should be data-driven;

- Raising the size of caps raises revenues for veYB (while 20% of YB inflation is irrevocably incentivizing crvUSD pools) and crvUSD trading volumes proportionally.