Summary:

Add gauge for the wstUSR-long LlamaLend market to the gauge controller.

This proposal includes an overview of Resolv wstUSR and rationale for the LlamaLend market configuration.

Abstract:

The wstUSR-long market has been configured similar to the sUSDS-long LlamaLend market, as it has similar properties and efficient redemption processes. One notable difference is the inclusion of a proxy oracle that allows the DAO to change the oracle implementation post-deployment. This may be necessary if liquidity migrates to new pools, making the original implementation an unreliable price source. The market also introduces a modified CryptoFromPoolsVaultWAgg oracle implementation that can chain multiple Curve pool price oracles + ERC4626 vault + agg price of crvUSD.

Resolv (wst)USR Overview

LlamaRisk has previously reviewed Resolv wstUSR and USR as part of Aave onboarding proposals. Those can be found here:

USR is a synthetic stablecoin backed by ETH, BTC, and stablecoins that employs delta-neutral strategies on short perpetual futures to maintain its $1 peg. Resolv facilitates the minting of USR and maintains systemic overcollateralization by managing a combination of hedging and staking strategies, and incorporating insurance mechanisms. It utilizes off-exchange asset custody with custodians such as Fireblocks and Ceffu, and conducts operations on several futures exchanges such as Binance, Hyperliquid, and Deribit.

USR can by staked as (w)stUSR to earn a portion of the rewards from protocol operations. wstUSR is a non-rebasing, ERC-4626 token compatible with DeFi integrations. A distinguishing feature of Resolv compared to analogous delta-hedging synthetic stables is that unstaking is instantaneous and USR redemptions are quite efficient ($5m daily instant redemption and 24hr redemption time for additional redemption demand). This is possible, in part, due to senior and junior risk tranching- RPL is a high yield liquid insurance pool that may absorb protocol losses, protecting the stability of USR and stUSR.

Collateral Management and Hedging Strategy

To preserve the USR peg and mitigate volatility in the collateral base, Resolv employs hedging strategies that involves opening short perpetual futures positions . This mechanism offsets exposure to downward price movements on volatile collateral types like ETH and BTC, thereby contributing to the stability of USR. This means that protocol stability is highly dependent on the reliable operations managed by the Resolv team.

- The collateral for these futures positions is securely held in custody by CEFFU and Fireblocks, mitigating the risk of exchange hacks/insolvencies that may otherwise impact protocol solvency.

- Details regarding exposure allocation to perpetuals and other strategies can be found here.

- In addition to futures, a portion of collateral is allocated to staking strategies, which are conducted transparently on-chain. The staking allocation is outlined here.

RLP Liquid Insurance Pool

Resolv maintains a target overcollateralization ratio for USR, with any excess collateral beyond this threshold allocated to backing RLP, a junior tranche asset that represents a share in the pooled collateral surplus.

- RPL receives a “Risk Premium” — a larger share of profits generated from perpetual futures positions compared to stUSR holders.

- RLP holders effectively act as the protocol’s insurance underwriters, absorbing performance-based risk in exchange for greater yield.

- Further details on profit distribution can be found here.

Minting and Redemption Mechanics

At present, USR can be minted by depositing USDC, USDT, DAI, or USDe. While minting fees may be introduced in the future, they are currently waived to encourage adoption.

Whitelisted users may redeem USR for the underlying collateral by first burning an equivalent amount of USR and paying a redemption fee (currently waived for all users). This process is completed within 24 hours, with $5m in instant daily redemptions, at present. This time window reflects the operational latency required to unwind staked assets and futures positions.

Risk Management and Disclosures

Resolv has compiled a list of risks involved in using their protocol, available here.

Key risk involved and their mitigations include:

- Counterparty Credit Risk

- Risk: Insolvency of a perpetuals venue could lead to significant losses.

- Mitigation: Use of reputable custodians (CEFFU, Fireblocks), diversification across venues, and the RLP insurance pool. The protocol may still experience losses in unrealized PnL in case of exchange insolvencies.

- Market Risk

- Risk: Negative funding rates for perpetual futures positions may erode capital.

- Mitigation: Use of highly liquid venues, and reliance on RLP to absorb volatility loss. This mitigation involves trust in the Resolv team to properly manage backing assets.

- Liquidity Risk

- Risk: Mass redemptions could lead to insolvency of USR or RLP.

- Mitigation: Protocol enforces a safeguard whereby RLP redemptions are suspended if USR’s collateralization ratio falls below 110%, preserving stability and solvency.

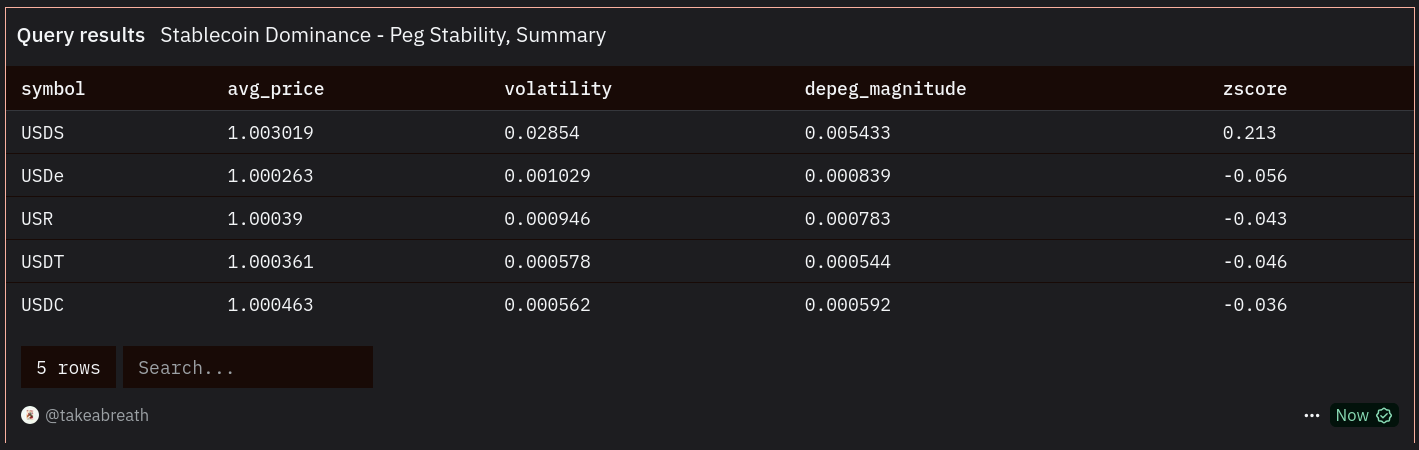

Peg Stability

We have compiled some summary statistics which describe the peg stability of USR compared to competing stable coins.

source: Dune

data sampled from date of USR deployment till time of writing

Whilst USR is one of the newer assets on this list, USR shows overall strong peg relative to others.

Specification:

Market Parameters

| Parameter | Value |

|---|---|

| A (Band Width Factor) | 300 |

| AMM Swap Fee | 0.2% |

| Liquidation Discount | 1% |

| Loan DIscount | 1.3% |

| Max LTV | 98% |

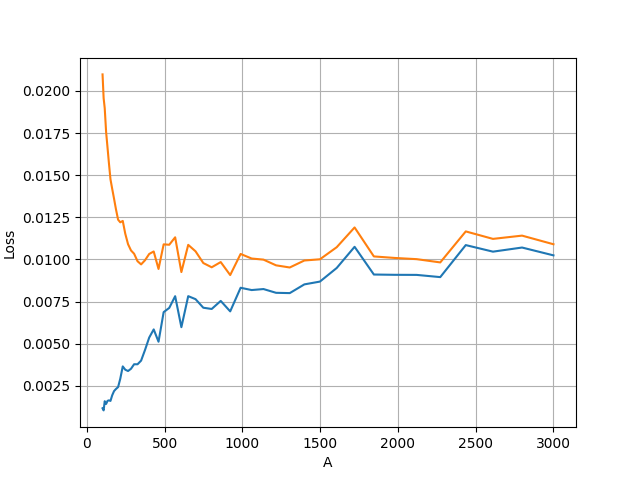

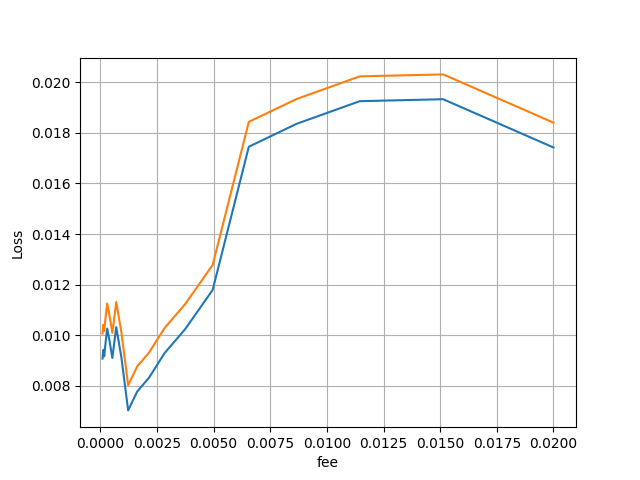

The market has been instantiated with the same market parameters as the sUSDS-long market in prod. USR is a relatively new product a short history available to refine specific attributes of this asset. However, given wstUSR has favorable redemption efficiency compared to other delta-hedging synthetic dollar protocols, the assumption of stable peg performance in normal protocol operation is reasonable.

For reference, we have run an optimization analysis for USR, which can be found below. The analysis suggests that the market can support more aggressive parameterization based on its market history. However, borrower losses are well contained at A=300 and we add additional buffer to the liquidation discount (1% instead of 0.5%) to allow for arbitrage in case of peg instability.

Monetary Policy

| Parameter | Value |

|---|---|

| Min Rate | 0.1% |

| Max Rate | 35% |

The market uses Semilog Monetary Policy, the current standard for LlamaLend Markets. This policy uses a polynomial curve based on the market utilization and the min/max rates set by governance. The parameter config has been set with a somewhat higher max rate compared to other yieldbearing stable markets (35% instead of 25%) and is intended to exceed the expected yield on the underlying, thereby protecting lenders against market illiquidity. While the all-time average staking APR is 8.68%, the most recent 7-day average is 12.59%, reaching at times over 20%.

Oracle

Proxy: https://etherscan.io/address/0x31624Ed311Fe6116011Aa297D3dEA6030e8Cf572

Implementation: https://etherscan.io/address/0x2850EeFBd921dfAb32d69abeD3D1aE819617C643

Both the oracle proxy and implementation are new with this market deployment. The proxy allows the DAO to set a new oracle implementation, if necessary, without requiring a market migration. The implementation CryptoFromPoolsVaultWAgg is an oracle that chains multiple curve pool price oracles with an ERC4626-compliant vault and the aggregated price of crvUSD.

The underlying pools and contracts used in the oracle include:

- USR/USDC : $8.4m TVL

- USDC/crvUSD: $34m TVL

- wstUSR vault

- crvUSD price aggregator

Resolv have indicated an intention to maintain the USR/USDC pool as a primary liquidity venue so that it will be a reliable oracle source for the foreseeable future. Note that this oracle configuration assumes that wstUSR maintains a peg to USR- this is considered a reasonable assumption because wstUSR can be instantly unstaked. In case an unstaking cooldown is introduced, this assumption would not hold true and may necessitate switching the market’s oracle source.

The use of aggregated price of crvUSD improves the resiliency of the market to instances of transient crvUSD depeg in the constituent pools. This reduces the probability that users can be liquidated as a result of crvUSD price deviations. Older LlamaLend markets do not include aggregated price of crvUSD, but it is now a standard for all future markets deployments.

Vote Actions

This vote is to add the wstUSR-long LlamaLend market to the gauge controller.

ACTIONS = [

# Add wstUSR-long gauge to gauge controller

("0x2F50D538606Fa9EDD2B11E2446BEb18C9D5846bB", "add_gauge", "0x91D0F7022edb620429B4F63D482fcfbb2cbE7F30", 0, 0),

]